After five straight weeks of losses on Wall Street, followed by last week’s “dead cat bounce“, the question I get asked more than any other is, “Thom, do you think we’re going into a recession?” The answer, as the title suggests, is increasingly and overwhelmingly yes, although many of the mismanaged causes now contributing to that recession have been entirely avoidable. As Forbes just reported, the last 10 weeks have been the fifth worst start to a year in U.S. stock market history, and many investors are appropriately rattled.

First, let’s start with a couple definitions. Inflation, as economists define it is “too many dollars chasing too few goods.” This begs two questions: The first, is “Where did all those excess dollars come from?” The second is, “Why do we have too few goods?”

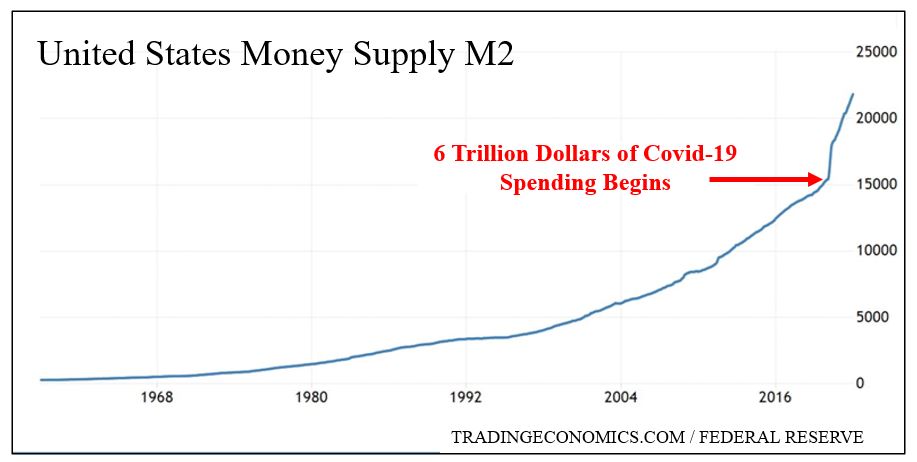

As you can see from the chart below, the Federal Reserve released an unprecedentedly massive amount of liquidity into the economy in response to the economic slowdown that occurred as a result of the self-imposed lockdowns on the strongest economy we’ve ever had, from February 2020 through the end of 2021, and that increase has only continued at a far steeper pace than at any time in our history. As logic dictates, if you double the amount of dollars in circulation, and the size of the economy remains constant, each dollar becomes worth half as much, requiring twice as many as previously needed to purchase the same basket of goods.

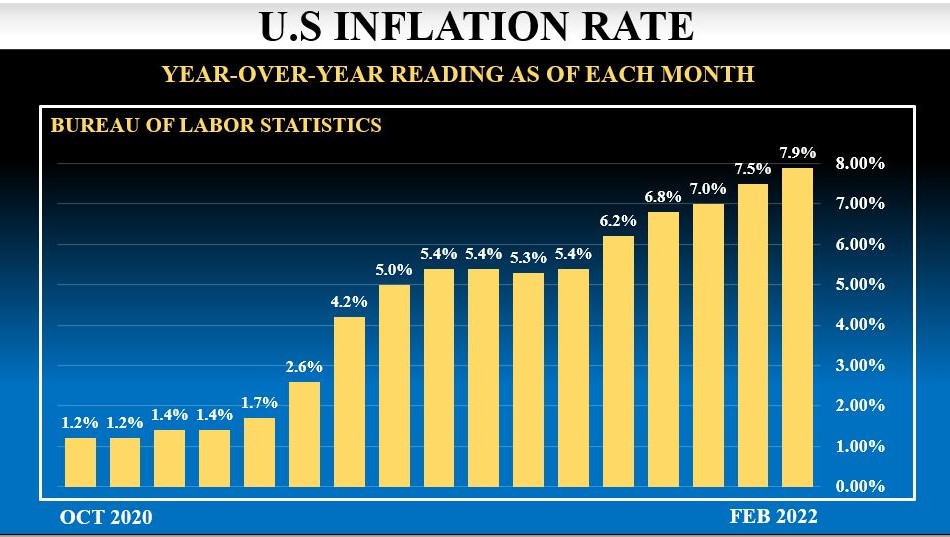

As to the reason we have too few goods, economists initially assumed, in part correctly, that this was due to the supply chain disruptions caused by the lockdowns as a response to the spread of Covid-19 worldwide. Happily, many of those disruptions have since remedied themselves, revealing an even bigger culprit that has been in place since the early days of the Biden administration, namely their well-documented, campaigned upon, unrelenting disdain for Western society’s reliance on fossil fuels. I’ll get to the widespread consequences of that in a moment. Suffice it to say that inflation has been obvious to all but The Economist, is far from “transitory” as the Fed initially claimed, is accelerating (see below), and is compounded by the increase in fuel costs that began during Biden’s first week in office, increases which have only intensified since Russia’s invasion of Ukraine.

After the new 7.9% year-over-year Consumer Price Index (CPI) number was released last Thursday, economist and money manager Peter Schiff put that figure into historical context: “If we used the same CPI formulation now that we used in 1982 (the last time we had inflation at these levels) we’d be over 15% inflation, not 7.9%. This is the worst inflation in our lifetimes… Inflation’s got only one way to go and that’s up…”

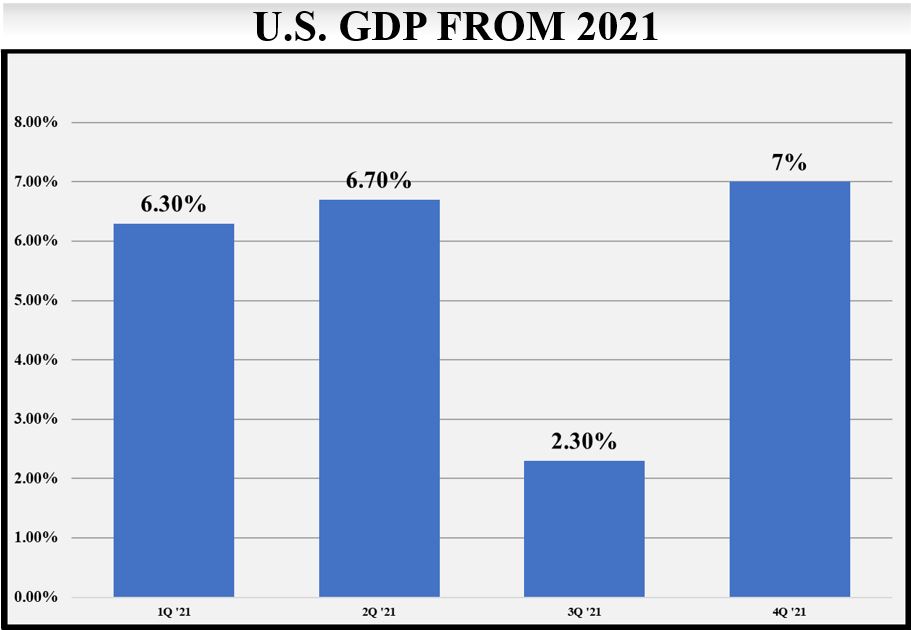

Having defined inflation, the second definition we need to address is that of a Recession: Two consecutive quarters of negative growth. As the chart to the right shows, last year’s recovery from the Covid pandemic was expectedly vigorous, given the aforementioned $6 trillion dollars that Congress, two administrations, and the Federal Reserve threw at the problem. Currently, the Atlanta Fed is reporting that the annualized pace of growth for the first quarter is only 0.5%, with only two weeks to go in the quarter and the economy clearly slowing as the war in Ukraine causes shortages around the world—from heating oil, to natural gas for fertilizer, potash, diesel fuel, gasoline, iron, grain, plastics, and a myriad of other products that much of the world depends upon but is now boycotting from Russia as a source.

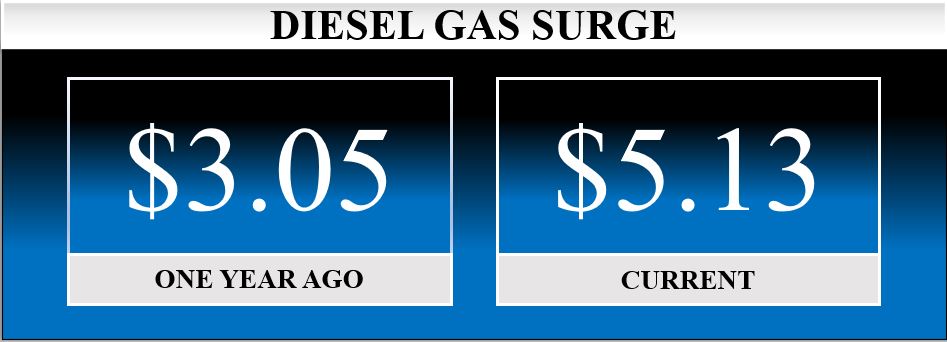

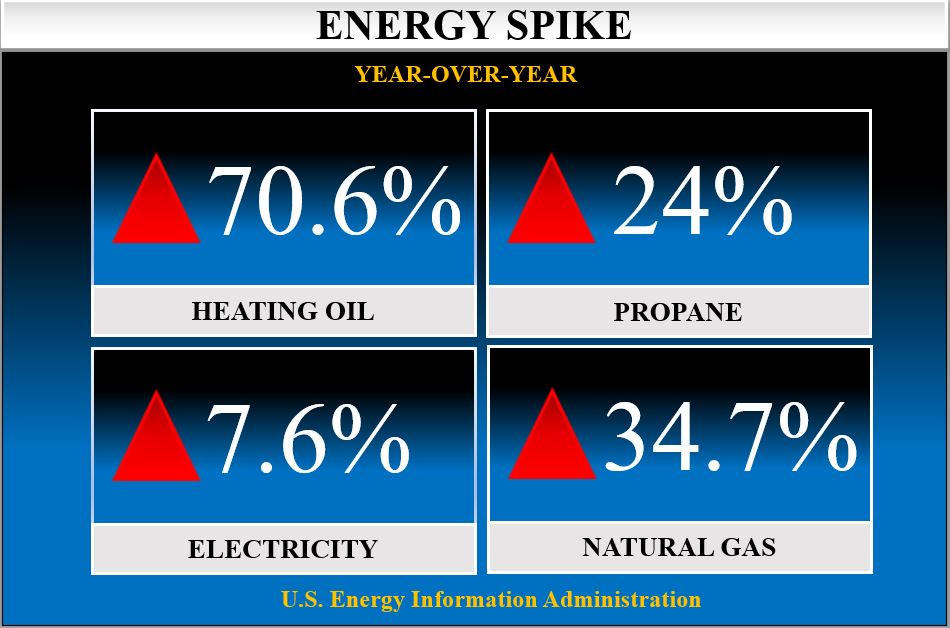

Although Russia’s economy is equal in size to roughly that of Texas, they are the world’s second leading exporter of fertilizer, especially potash, a key ingredient used on major commodity crops and produce around the world. US-based Mosaic Co., a major fertilizer producer, just warned of potash shortages, and lower crop yields per acre as the spring planting season approaches. This could be a harbinger of international food shortages later this year, especially when combined with the increase in the cost of diesel fuel from $3.05 per gallon a year ago to $5.13 (+68%) last week. Over 70% of American goods arrive on store shelves throughout the nation via 18-wheelers owned by independent operators who rely upon stable diesel prices.

Finally, natural gas is a key component in producing fertilizers since a basic component thereof is methane. Indeed, so many industries are intricately related, as well as dramatically harmed by a spike in the cost of natural gas—up 35% in the last year—and impact the production of plastics, rayon, polyester, the cost of refrigeration (propane, up 24%), along with “cookers, ovens, clothes dryers, and central heating…” When so many of the items that we depend upon in our daily lives are 24 to 68 percent more expensive—and the cost of delivering those goods to store shelves throughout the nation is 70% higher than it was a year ago, a prolonged recession is inevitable.

The longer Putin persists in his invasion of Ukraine, the more the West digs in with their punitive sanctions, the worse all of this gets and the longer the recession will last. Biden’s ongoing refusal to ask our domestic energy industry to once again ramp up production, while asking Venezuela, Saudi Arabia, and—shockingly—even Iran for oil instead is shamefully inept, tone-deaf, and punitive to the average American household. Each of those countries produce far dirtier oil—with far fewer environmental safeguards—than we do here in the United States, thus eliminating the environmental justification for such stupidity. (This is the local equivalent of posting a “No Urinating” sign at one end of the town pool, while allowing parents to empty their toddler’s soiled diapers into the other end—it’s literally that ridiculous.) If global climate change is to be combatted globally, our purchase of dirtier oil from dictators, theocrats, and terrorists isn’t solving the problem, it’s making it worse.

All of this, of course, follows the country’s national embarrassment over the incredibly botched Afghan withdrawal last year, a fiasco so mismanaged that our incompetence signaled weakness to that same Iran, Russia, and even China, each of whom has since stepped up their nefarious activities around the globe. Remember that it is China who is watching the U.S./NATO response to Putin’s war crimes in Ukraine, even as their multiple recent violations of Taiwanese airspace signal their intentions there in the coming months. Were a Chinese invasion of Taiwan to succeed with no consequence from the United States, China would control over 92% of the world’s 5G advanced microchip production, giving it both an industrial and a military monopoly from which the U.S. would likely never recover. The geopolitical stakes for the world couldn’t be higher, and the administration’s responses to all of these events have been weak, naïve, and wishful at best.

As of this writing, at least 31 Democrats in Congress have announced they will not be seeking reelection in the upcoming midterms in November. Apparently, these folks are capable of reading the tea leaves and know that the future of the Pelosi/Biden agenda is very much in doubt, and that our weakened president is already a lame duck in practice. The last time the party in power in both Congress and the White House faced such daunting losses, the Republicans led by Newt Gingrich were swept into power for the first time in over 40 years. Markets loved it, because gridlock ruled the day. From 1994 to 2000, we had divided government. Nothing passed unless there was a broad consensus for its passage, the tax code saw minor improvements, and President Clinton realized that he had to “go along to get along”, even declaring that “the Era of Big Government is over” during the 1996 State of the Union address.

Investors don’t like change. They like steady, level playing fields. Although the threat of the repeal of the Trump tax cuts of 2017 still remains, that threat is reduced significantly in light of Biden’s weakness and multiple distractions around the world. While it may take some time, perhaps longer than usual to come out of the inevitable recession ahead, long-term investors can take solace from the gridlock ahead.

Those of you entering retirement, or newly in retirement—or for whom retirement is just a few years away—would be wise to consider protecting some of the incredible gains of the last 14 years. War is a tricky business, and there are no guarantees, and we already know that Putin’s appetite for war crimes knows no limits. The West finds itself atop a slippery slope, and prudence is the operative sentiment. Today we are but several bad days in Ukraine from a bear market in U.S. stocks and historically the average bear market sell-off of the last 80 years is a decline of -41%. Market timing is a fool’s errand, and fear-of-missing-out, a/k/a greed, was last year’s strategy.

Remember: “The only thing we’ve learned from market history, is that investors continually refuse to learn from market history.”

2 Comments

Thom, this is an excellent piece. Your explanation and analysis were clear and concise and a comprehensive view of where our country stands today.

Susan

Thanks Susan. I marvel at how much the world has changed in just two years, and how our core institutions are in jeopardy from an indifferent public with no concept for the price that others have paid for the freedoms they seem so willing to toss aside.

I always appreciate your and David’s comments!

Best,

Thom