Sugar is up 50%, gas prices are up $1.10 this year, and lumber (was) up over 300%. Many of you have been emailing and calling asking, “Should we be worried that 1970s style inflation is back?”

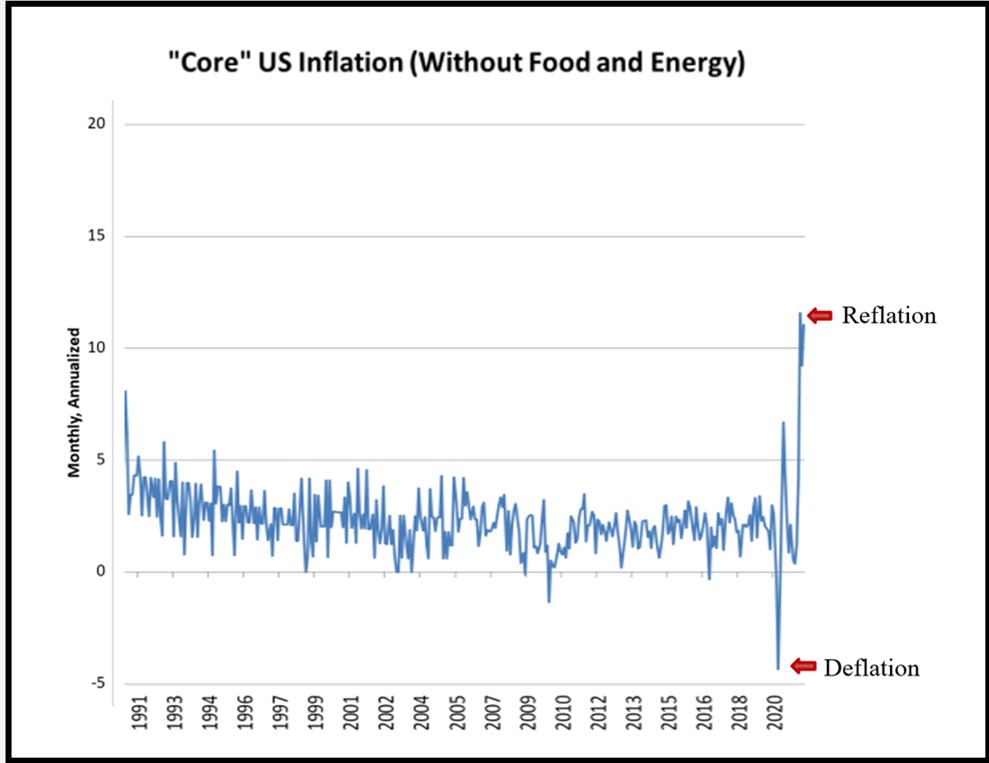

As I’ve been saying on my radio show for several months, if the markets actually believed that these inflation numbers were anything to worry about, we wouldn’t still be testing all-time highs on a weekly basis. The reason the year-over-year Producer Price Index—up an astonishing 7.3% in June—is so pronounced this time around is a statistical anomaly, rooted in the fact that they were so low exactly one year ago, something you can see in the far right side of the graph below.

Similarly, U.S. retail sales were up a whopping 18% year-over-year last month, but nobody believes that is sustainable, and we all understand that it’s because retail was effectively shut down last summer amid a nationwide lockdown.

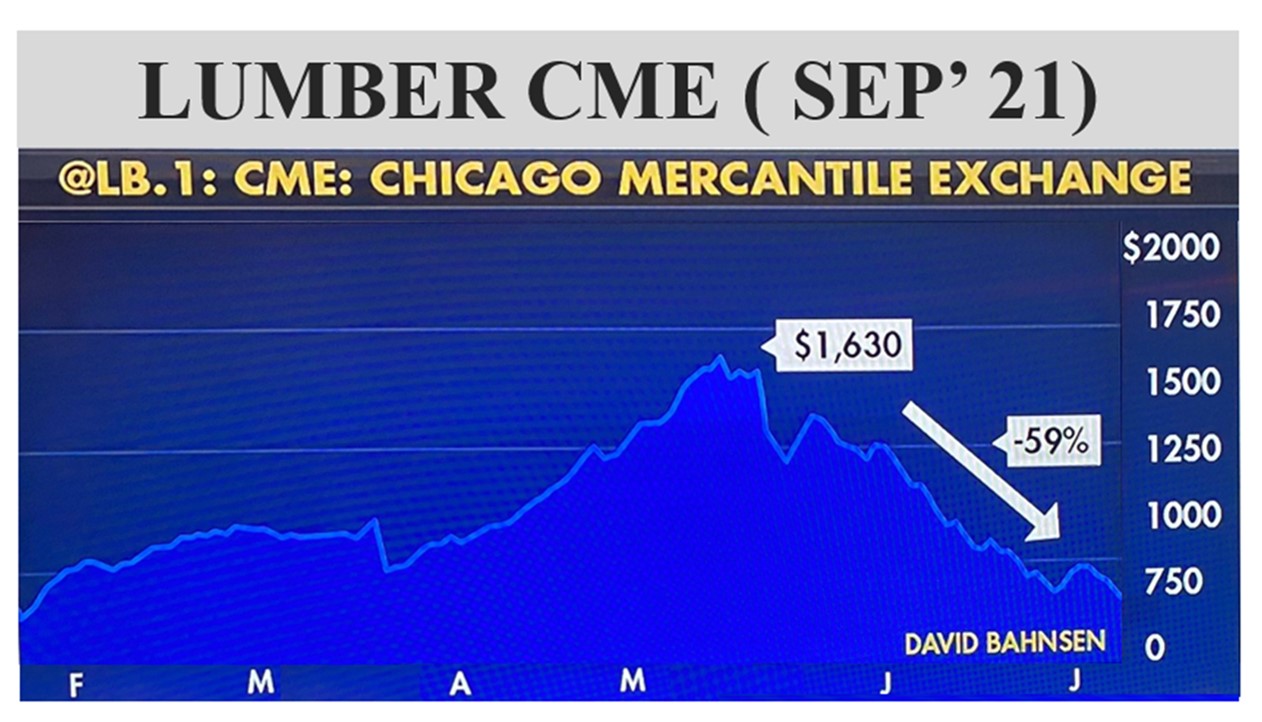

Lumber prices, which were recently up over 300% through the end of April, are now down -59% from that high, as reported by Larry Kudlow last Tuesday. This means that from their pre-pandemic lows, lumber prices are now up only 64%, still an enormous increase in 17 months, but dropping.

Like lumber, much of the rest of the inflation in the economy is a function, not of product shortages, but labor shortages. Because a Covid-sympathetic Congress passed a $300 per week supplemental unemployment benefit that is scheduled to continue through September 6th , laid-off employees can make more money at home on enhanced unemployment than if they returned to their former jobs. Their employer’s single biggest complaint with the reopening economy is that they lack the labor to staff their accelerating demand. With lumber, we haven’t had a shortage of trees, we’ve had a shortage of sawmill employees, plywood lamination technicians, and truck drivers to drive the finished millwork to the lumberyards. We’re seeing the same thing with agricultural demand, which was down dramatically amid the closure of restaurants, cruise lines, and hotels worldwide during the pandemic, but is now straining under the pent-up demand of people booking cruises again, booking airfares, and eating out in droves.

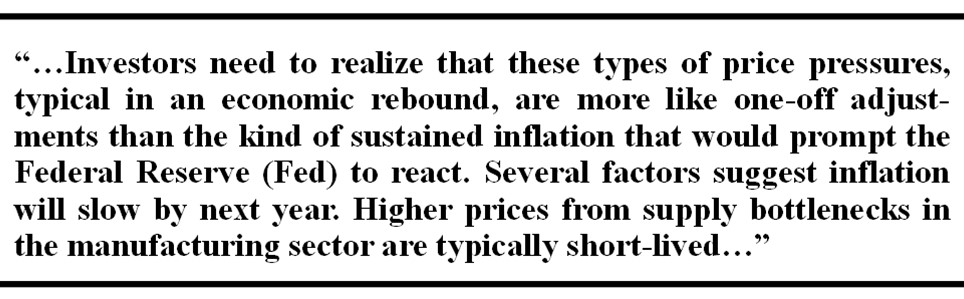

Scott Minerd, the CIO of Guggenheim Partners, is the single most respected/requested speaker at Jackson Hole and Davos every year, when the world’s central bankers get together to discuss the global economy, interest rates, monetary policy, and global GDP. Guggenheim is world-renowned for their research, and that research is not buying the inflation fears of the panicked economic media. Scott wrote this over 2 months ago, and is continuing to maintain this position with additional data:

This past Thursday, Hank Smith of the Haverford Trust Company, was on Fox Business making a similar point:

“…The forces that have kept inflation at bay for 25 years now are still present, those being globalization, demographics, and technology—and those trends aren’t changing. So we do have inflation right now, but that is because we had a deflationary economy a year ago. Let’s call this reflation instead…”

Economists and market watchers can be divided on whether inflation is transitory or not, but a close examination of the economic data favors the former. Whether this temporary anomaly fuels longer-lasting wage inflation still remains to be seen.

2 Comments

Thom,

I really appreciate your analysis and logic. Thank you so much for sharing what many of us intuit, but you put it in understandable facts.

Karen

Thanks Karen. I appreciate the compliments and am glad that you’re enjoying the information.

Best,

Thom